Kevin O'Leary recently said that nine-to-five workers have no place in his organizations. He argues that remote work made traditional hours obsolete. Mark Cuban tells you to work as if someone is grinding 24 hours a day to take everything away from you.

That advice sounds intense. It also sounds increasingly out of touch.

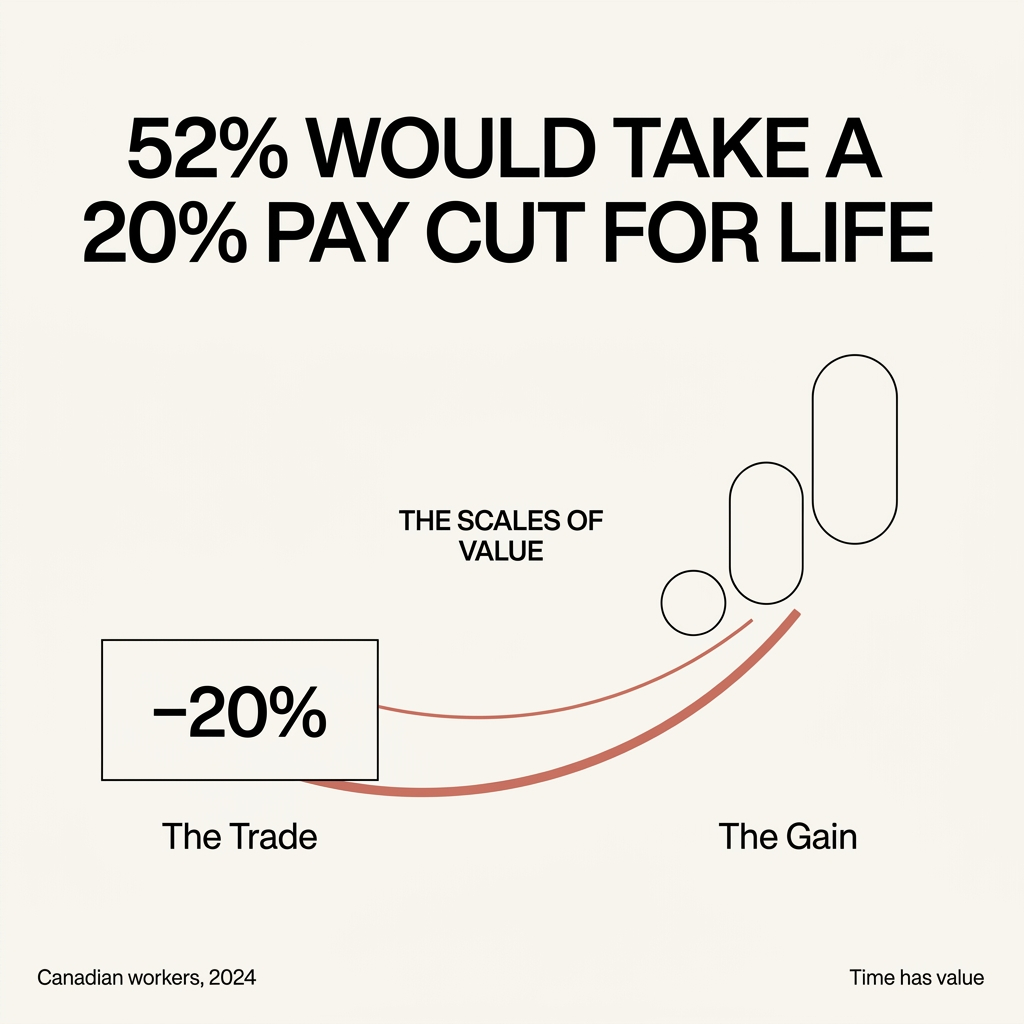

Because while billionaires talk about unlimited availability, workers are quietly running a very different calculation. In Canada, 52% of workers say they would accept a 20% pay cut in exchange for a better quality of life.

Half the workforce is willing to trade real money for time. That is a signal worth investigating.

The Gap Between the Podium and the Payroll

When someone worth billions gives career advice, it carries weight. It shapes hiring norms, management expectations, and how you judge your own work ethic.

Here is the problem. The advice is optimized for a very specific goal: extreme wealth accumulation. Building a billion-dollar fortune requires trade-offs that almost nobody is actually trying to make.

You are probably optimizing for something else. Financial security, time with family, health, a career that lasts 40 years without burning out at year 12.

Following hustle-culture advice when your goals are different is like using a marathon training plan to prepare for a casual weekend hike. The plan works. It was just built for a different race.

💡 Key insight: Advice is only as good as the goal it was designed for. Before adopting anyone's work philosophy, check whether their finish line matches yours.

What the Data Actually Shows

Strip out the opinions and look at the measurements. The Canadian workforce is giving us an unusually clear picture right now.

Life Satisfaction Is Falling

Among Canadians aged 15 and older, life satisfaction dropped from 54.0% in 2021 to 48.6% in 2024. General unhappiness has doubled since 2015, reaching 36%.

A decline this broad points to a systemic issue. Individual bad luck does not double a national unhappiness rate in nine years.

Work Stress Has Become a Health Issue

The mental health numbers make the connection to work explicit:

35% of Canadian employees report excess stress and anxiety

76.3% say work pressures negatively affect their mental health

When three out of four workers report psychological harm tied to their jobs, you are past the point of individual coping strategies. This is a public health pattern, and it carries economic consequences in productivity, absenteeism, and turnover.

Workers Are Repricing Their Time

The willingness of 52% of workers to give up 20% of their pay reveals something economists have long theorized: beyond a certain income level, additional money delivers diminishing returns compared to time and reduced stress.

This is commonly overlooked in compensation planning. Employers keep assuming money is the primary lever. The workforce is telling them, in measurable terms, that the calculation has changed.

The Demographic Warning Signs

The dissatisfaction is unevenly distributed, and that distribution matters for anyone running a business.

Younger adults and racialized Canadians report significantly lower life satisfaction than other groups. These same groups will make up a growing share of the workforce over the next two decades.

⚠️ For business leaders: If your culture depends on hustle expectations that these groups are already rejecting, you are building your talent pipeline on shrinking ground. The companies that adapt their work models now gain a durable recruiting advantage.

Think of it as a slow-moving supply problem. The supply of workers willing to sacrifice well-being for a paycheck is contracting, year by year, cohort by cohort.

Remote Work Cuts Both Ways

O'Leary's framing deserves a closer look. He says remote work made the nine-to-five obsolete. Read that carefully and you see the implication: if work can happen anywhere, work can happen anytime.

Technology that was supposed to give you flexibility becomes a mechanism for unlimited availability. The boundary that used to protect your evening dissolves when your office lives in your pocket.

This helps explain why the stress numbers climbed even as flexibility increased. Flexibility without boundaries expands the workday. The lesson for you as a worker, and for anyone managing a team, is that remote arrangements need explicit limits to deliver their intended benefit.

Working Less Without Earning Less: The Practical Playbook

Here is where the analysis gets useful. Rejecting hustle culture does not require accepting financial insecurity. The smarter move is optimizing your income-to-time ratio. Four strategies stand out.

1. Raise Your Hourly Value Through Skills

The fastest way to work fewer hours at the same income is to make each hour worth more. High-demand skills in areas like data analysis, project leadership, and specialized trades command premium rates.

Six months of focused learning can reprice your time permanently. That is a better return than six months of extra overtime.

2. Move to Better-Compensated Fields

Some industries simply pay more for the same effort and hours. A deliberate career transition, planned over one to two years, often does more for your quality of life than a decade of grinding for incremental raises in a low-margin field.

3. Build Passive Income Streams

Dividend investing is the clearest example from the data. A portfolio yielding around 6.55% turns a $10,000 investment into income that arrives whether you are at your desk or at the lake.

Small at first, yes. Compounded and added to consistently, passive income gradually replaces hours you would otherwise have to sell.

4. Negotiate Flexible Arrangements

Compressed weeks, hybrid schedules, and asynchronous work can save you 20 to 30 hours annually in commuting and idle office time alone. Those hours are real economic value. Claim them in negotiations the same way you would claim salary.

Success Is Being Redefined, Quietly

Put the pieces together and a larger shift comes into focus. A growing group of workers is redefining success as optimized life satisfaction rather than maximum earnings.

Some observers call this the rise of the quietly wealthy. These are people who build sustainable financial security through skills, passive income, and deliberate boundaries, then stop climbing when the returns no longer justify the cost. They skip the visible status race entirely.

The willingness of a majority of workers to trade 20% of their pay for quality of life represents a philosophical shift, one that challenges the assumption that financial maximization is the primary human motivator.

There is also a macro dimension worth watching. Mental health metrics are starting to function as leading economic indicators. Societies and companies that protect worker well-being position themselves for long-term gains in productivity and innovation. The ones that extract maximum short-term labor pay for it later in turnover, disengagement, and health costs.

What You Should Take From This

Three practical conclusions come out of this data.

If you are a worker: Run your own numbers before adopting anyone else's work philosophy. Calculate what an hour of your time is worth to you, in money and in well-being. Then use the four strategies above to improve that ratio deliberately.

If you are a manager or founder: Treat the 52% pay-cut statistic as market intelligence. Flexibility, boundaries, and reasonable hours are now compensation. Companies that price them in will win talent that competitors chase with cash alone.

If you are evaluating advice: Check the source's goals against your own. Billionaire work philosophies are honest reflections of what it took them to reach the top 0.01%. The data shows that applying those philosophies to an ordinary career produces the costs without the proportional rewards.

The workforce has already voted, in surveys and in behavior. Time has value. Well-being has value. Smart careers, and smart companies, are the ones that account for both.

Start with one step this week. Audit your hours, price your time, and identify the single change, a skill, a negotiation, or an investment, that improves your income-to-time ratio the most. That is how you work smarter while the loudest voices keep telling you to work more.